Posted on January 27, 2023

Consider ways to help reduce taxes on your income and investments by acting now.

Key takeaways

- Wider tax brackets, a higher standard deduction, and expanded saving opportunities may help create new tax-saving possibilities for 2023.

- Don’t wait until the end of the year. There are tax-planning strategies to consider throughout the year, like maximizing credits and deductions and using tax-smart investing strategies.

- A tax advisor and financial professional can help you build a tax-smart investing plan that works for you all year long.

As we turn to 2023, there are plenty of uncertainties. Will the Fed engineer a soft landing for the economy? Will inflation slow? Will the stock market revive? Will interest rates come down? During uncertain times like now, it’s valuable to focus on things we can control—taxes, for example. While you generally can’t avoid taxes, you may be able to minimize them with a bit of thoughtful planning.

Here are 7 tax-smart steps to consider early in the year that are designed to help you keep more of your money—and put your savings in a position to grow too.

1. Seize available deductions

This year there is some good news for taxpayers. The IRS has widened tax brackets—meaning potentially lower income taxes for many—and increased the standard deduction and many savings incentives.

Inflation adjustments to tax brackets mean people may have more taxable income before being bumped into a higher tax bracket. Additionally, the standard deduction will rise to $27,700 for married couples, an increase of $1,800. For single filers, it increases by $900 to $13,850.

Consider your possible itemized deductions this year. The major ones included state and local taxes, medical and dental expenses, home mortgage interest, charitable donations, and deductions for casualty and theft losses from a federally declared disaster. If you think these may exceed the standard deduction, you may want to consider bunching enough deductions into 2023 to capture a larger write-off by itemizing deductions.

Itemizers can also donate appreciated assets held longer than one year to a qualified public charity and deduct the fair market value of the asset without paying capital gains tax. The donation is generally subject to a 30% adjusted gross income limitation. Any excess deductible amount can be carried over for up to 5 years.

2. Make the most of higher saving incentives.

If you haven’t contributed to an IRA, health savings account (HSA), or 529 college saving account for 2022 you have until April 18 of 2023 to do so. But if you know how much you’d like to contribute for the year, also consider making 2023 contributions earlier in the year, giving you more time to grow your money tax-deferred.

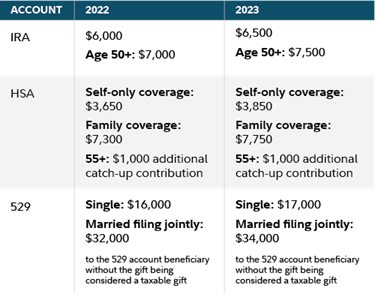

- IRAs: You can contribute $6,500 to an IRA for tax year 2023, up from $6,000 for tax year 2022. And if you’re over 50, you can contribute an additional $1,000 per individual.

- HSAs: If you are eligible to contribute to an HSA, contribution limits are $3,850 for self-only coverage and $7,750 for family coverage for 2023, with $1,000 more in catch-up contributions for those 55 and over. That’s up from $3,650 for self-only coverage and $7,300 for family coverage in 2022, with no changes to the catch-up contribution for individuals age 55 and older

- 529s: If you have children, grandchildren, or are considering further education for yourself, consider contributing to a 529 college savings account, where any growth accrues potentially tax-free. While aggregate contribution limits to 529s are governed by state tax laws and are usually quite high, individuals may contribute up to $17,000 ($34,000 per married couple filing jointly) to any number of recipients in 2023, likely without it being considered a taxable gift. That’s up from $16,000, and $32,000 per married couple filing jointly in 2022.

Contributions to a traditional IRA or HSA may reduce your current taxable income, as long as you are eligible to contribute and to take a deduction. You can also make a Roth IRA contribution. It’s important to note, however, that traditional IRA and Roth contributions are aggregated and can’t exceed the annual limit. Although contributions to a Roth are not deductible, any earnings growth can be withdrawn tax-free, if you meet the income requirements and follow the distribution rules.1

3. Put your savings to work

If you were able to sock away extra savings in the last few years, you may want to put those dollars to work for you with tax-efficient investing.

(Try Fidelity’s calculator to determine the potential impact bunching donations may have on your taxes.)

In any market, there are opportunities to grow your money. This year, the stock market may be more challenging. But rising interest rates have provided opportunities in individual bonds and certificates of deposit (CDs). Where you hold those assets can also help you keep more of your earnings after tax. In line with your portfolio level asset allocation, holding investment products that generate interest income taxable at income tax rates, like bonds and CDs, in tax-deferred accounts like IRAs can help minimize taxes. On the other hand, stocks, where long-term gains are taxed at lower capital gains rates, may be better held in taxable accounts.

For more on tax-efficient asset location, read: Are you invested in the right kind of accounts?

If you have money to donate, you have many strategies to consider for the 2022 tax year. You can’t take a deduction for most charitable contributions while also claiming the standard deduction. However, if you itemize, you generally can claim a portion of your donation as a deduction. It may make sense to try to bunch your charitable donations into a single year to maximize your potential deduction, and you could create a plan to do that for 2022. (Try Fidelity’s calculator to determine the potential impact bunching donations may have on your taxes.)

4. Tax-loss harvesting

For nonretirement accounts, you might also want to consider year-round tax-loss harvesting where you use realized losses to offset gains, plus up to $3,000 of ordinary income depending on filing status. If you’ve got investments that are below their cost basis, and there’s another investment (but not a substantially identical security), you could use it to replace the sold asset without a material impact to your investment plan. Consult your tax advisor about your situation and beware of the wash-sale rule. One exception is cryptocurrency—wash-sale rules currently do not apply to cryptocurrencies, as they are not regulated as securities. That means you can sell coins whose value has declined, and buy them back immediately at the same price, potentially realizing the loss while still holding the asset. Pending legislation about cryptocurrency regulations may eliminate this loophole, so be sure to work with a tax professional to stay on top of changes.

5. Consider a Roth conversion

A Roth conversion involves transferring money in a traditional IRA to a Roth IRA, and then paying taxes on the converted amount. After that, the money grows and can be withdrawn tax-free,2 and it’s not subject to a required minimum distribution for the life of the original owner, generally once you have met the 5-year aging period. (A spouse who is the sole beneficiary of a deceased spouse’s Roth IRA also does not have to take an RMD from the account, if they roll it over into their own Roth IRA.) Now may be the time to consider a Roth conversion; with many investments down this year, you can convert more shares for the same total amount and same potential tax bill. Also, tax rates are set to increase in 2026, so you could end up paying higher rates if you wait to convert your traditional IRA until 2026.

6. Do a checkup

Doing a financial checkup periodically throughout the year can help you to pay the right amount of taxes as you go. The IRS has a handy tool Opens in a new window to help taxpayers check their federal income tax withholding. Consult your state tax authorities to check your state tax withholding.

You can also potentially reduce your tax burden if you take the time for some thorough bookkeeping to make sure you’re claiming all the deductions and credits that you can.

One potential area for adjustment, given that remote work may be here to stay for many workers, is to take a close look at your residence. If you are still working remotely in a lower tax state from where you usually work, you may want to take a deeper look at your residency options and make a long-term decision about the best choice for your situation.

7. Revisit your estate plan

Time is running out on the 2017 Tax Cuts and Jobs Act (TCJA), with estate planning provisions, scheduled to sunset at the end of 2025. That means the estate and gift tax exclusion, which was doubled, could revert to its pre-2017 level. You might consider accelerating gifting or donating appreciated assets. You can gift up to $17,000 per donor to as many individuals as you like, and if you’re married, each person in the couple can gift this amount without the gift being considered taxable.

Bottom line

Tax planning is not a one-and-done exercise. To help reduce taxes, it makes sense to be planning throughout the year. Need help? A tax advisor and financial professional can help you build a tax-smart investing plan that works for you.

Source: https://www.fidelity.com/learning-center/personal-finance/tax-moves

FIDELITY VIEWPOINTS 12/12/2022

Recent Comments