Posted on May 23, 2024

When it comes to planning for retirement, determining your personal identity—and associated goals—is an important (and often overlooked) step.

Jeff Montgomery, 70, has always been an active, highly engaged person—and he’s no different in retirement.

Upon retiring at age 63, the former managing partner of a London private equity firm first transplanted his wife and teenage daughter to Tokyo and immersed himself in Japan’s jazz scene, a pet interest. Afterward, the family relocated to Colorado, where they rebuilt a ski chalet into a full-time residence. “When your identity is all about ambition and working toward a goal, you can’t just give that up,” he reflects.

Jeff’s high-achieving version of retirement, which also includes serving on charitable boards, is not for everyone. However, it does raise an important question: What do you want your retirement to look like—and how much planning have you done to realize it?

“Retirement planning doesn’t begin and end with the size of your nest egg,” says Justin Richards, CFP®, CWS®, a Colorado-based senior financial planner for Schwab Wealth Advisory. “It’s just as important to consider how you’ll spend your time, especially given the extra hours you’ll gain once you stop working. Without a plan, many retirees can feel aimless and unfulfilled.”

But how do you begin to plan the retirement that’s right for you? While everyone’s experience is unique, retirees often fall into one of five categories. Read on to discover which type most resonates with you—and what to consider as you near and enter retirement.

The Dynamo

You love your career, and you pride yourself on being productive and useful.

According to the Pew Research Center, roughly 20% of adults ages 65 and older are still employed.1 “I have a client who’s 79 years old and still a practicing lawyer,” Justin says. “He’s invested 100% in stocks because he never wants to quit working and is mainly concerned with leaving a legacy.”

Full- or part-time work can deliver a sense of purpose—to say nothing of extra income, which can help extend your retirement savings. Jeff, for example, consulted for his old firm for five years after resigning his partnership in 2017. “Consulting allowed me to remain engaged while still leaving time for family and new projects,” he says.

Be that as it may, working in retirement can affect:

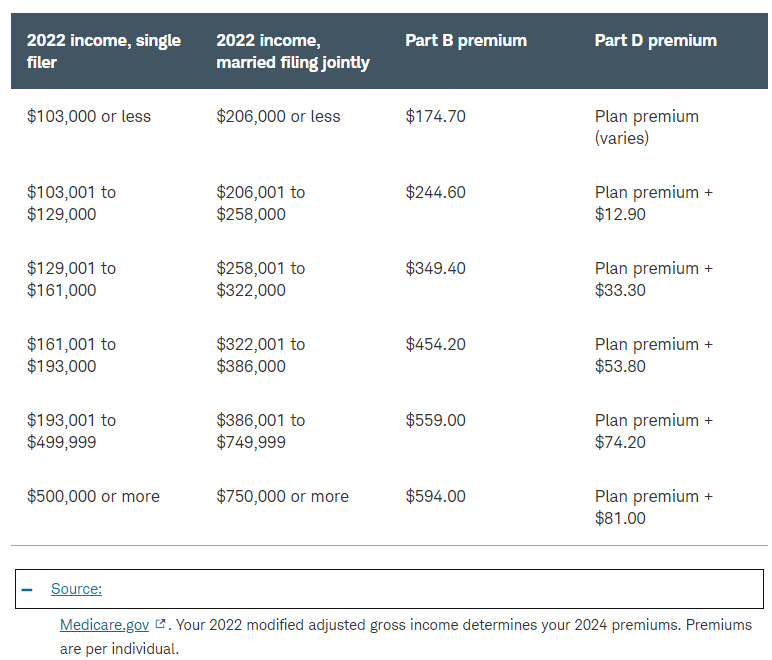

- Medicare premiums: Although retirees generally don’t pay premiums for Medicare Part A, which covers hospitalization, they typically pay premiums for Part B, which covers outpatient visits, as well as Part D for private prescription drug coverage—unless they’re covered under a qualified employer health insurance plan. The additional earnings can push those premiums up if your total annual income exceeds certain thresholds, though you may be able to appeal the increase after you retire.

A premium on premiums

The higher your income, the more Medicare Part B and private Part D coverage will cost.

- Pension benefits: Working part-time may influence your pension payout, which typically is calculated using your average salary for the last three or five years of work. If your part-time income is significantly less than your full-time income, you could see a drastic reduction in your benefit.

- Social Security benefits: Starting in the month you reach full retirement age, there’s no limit on how much you can earn and still receive your full benefit. However, if you collect benefits prior to reaching your full retirement age (between 66 and 67, depending on birth year), your payouts could be reduced. For example, if you’re under full retirement age for all of 2024, your benefits will be reduced by $1 for every $2 you earn above the annual limit of $22,320.

“If you have ample retirement savings and don’t need the income, you might consider whether something like volunteering your time makes more sense,” Justin says (see “The Philanthropist”).

The Adventurer

You stay active, are in good health, and have always wanted to fill up your passport pages.

“Today’s retirees generally are healthier, live longer, and want to do more than their predecessors,” observes Kate Goesel, CFP®, a senior manager with Schwab’s Centralized Planning Group in Chicago. “But the more you do, the more money you may need to do it, especially as it pertains to travel.”

A common rule of thumb is to plan for your retirement expenses to equal 80% to 100% of your current expenses. If you have big travel plans, however, you may need upwards of 120%, at least in your early retirement years.

To help foot the added costs, retirees who plan to travel extensively often downsize or move to a lower-cost city.

Retirees traveling internationally should also beware that Original Medicare typically won’t pay for health care expenses incurred outside the U.S. While some Medicare Advantage and Medigap plans may offer coverage abroad, you may need to budget for additional travel insurance that covers emergency medical expenses.

The Philanthropist

You enjoy giving back and want to dedicate more of your time to worthy causes.

Roughly a quarter of U.S. retirees spend part of their time volunteering, lending their connections, experience, and knowledge to nonprofit organizations. “These acts of service often provide a renewed sense of purpose and a new source of joy for retirees,” Justin says.

There are generally two ways to volunteer your time:

- Make a regular commitment: “Enlisting in a regular shift at a local charity is an ideal fit for people who are ready to retire but still want to remain active,” Kate says. However, be aware that volunteer hours are not tax-deductible.2

- Serve on a board: Those with corporate experience often find they can leverage those skills by serving on a nonprofit board. Nevertheless, many organizations require board members to make a financial commitment, either personally or through fundraising. If you’re not willing or able to meet that expectation, supporting the organization in another way may be a better option.

The Homebody

You’re done with work, and you dream of gardening, golf, and grandkids.

For many people, retirement means fully decompressing from a lifetime of work. “Not everyone is looking for a second career or monthslong travel,” Justin says. “Some people just want to enjoy a quieter life at home.”

If your vision includes hours in the garden or long walks around your neighborhood, your home should reflect those desires. “Relocating is a common part of the retirement puzzle, whether to be closer to family, reduce living expenses and taxes, or live in a more walkable location,” Kate says.

However, if your current home is right where you want to be, you may still need to age-proof it. The National Association of Home Builders (NAHB) recommends consulting with an occupational therapist and a Certified Aging-in-Place Specialist (CAPS), who can recommend common features to consider, such as widening doorways for wheelchair access or installing handrails, particularly in bathrooms.

“There’s also a movement among retirees to build guesthouses, or accessory dwelling units, on their properties,” says Anna Sinatra, CFP®, CWS®, a financial planner for Schwab Wealth Advisory in Phoenix. “Doing so allows them to rent out the dwellings for extra income in the early years of retirement—and provides an easy place to house a live-in caregiver should the need arise.”

The Joiner

You value community and want a curated retirement experience.

Resort-style retirement communities are growing in popularity—and it’s not hard to understand why. The Villages in central Florida, for example, has more than 50 golf courses—as well as basketball, bocce, swimming, tennis, and, of course, pickleball—along with social clubs and entertainment complexes. There’s something for everyone.

Such amenities might seem superfluous to some, but residents of retirement communities report better emotional, intellectual, physical, and social wellness than those who live in the community at large.3 Plus, independent-living communities typically offer a more maintenance-free lifestyle, with some including housekeeping, meals, and even transportation.

For retirees who enjoy an active, independent lifestyle but have an eye on the future, life plan communities (often called continuing care retirement communities, or CCRCs) can offer the best of both worlds. They offer independent living as well as access to higher levels of care—such as assisted living or skilled nursing—on an as-needed basis.

Of course, life plan communities often have costs to match their utility, with average entrance fees of $402,000 and rents that average more than $3,500 per month, according to the National Investment Center for Seniors Housing & Care. More amenities or a higher level of care usually means higher monthly costs. That said, the IRS may recognize a percentage of both the entrance fee and monthly fee as a medical expense deduction.

“Clients who don’t wish to rent their home or keep it as an inheritance asset sometimes sell their real estate to assist with funding entrance fees,” Justin says. In that case, you’ll want to understand the potential capital gains liabilities of selling your home. Simply subtract your cost basis (the price you paid for the house, plus closing costs and outlays for major improvements) from the sale price. You’ll be able to exclude the first $250,000 in profit ($500,000 if married filing jointly) from the sale, provided it’s your primary residence, you’ve owned it for at least two years, and you have lived there for at least two of the past five years.

Start early

“Although I decided at age 60 that I wanted to retire at 63, the planning started 20 years earlier,” Jeff Montgomery recalls. “My retirement wasn’t a single event but rather a slow and steady process that included not just the right financial advisors but also building friendships and a sense of community.”

“Don’t wait until you get to retirement to start thinking about what you want from this next phase of life,” Kate says. “The sooner you start planning, the more time you have to fine-tune your vision—and adjust as necessary to help make your dreams a reality.”

https://www.schwab.com/learn/story/what-kind-retiree-will-you-be

May 16, 2024

Recent Comments